Fragile footing: How India, China face sizeable economic damage prospects from US-Iran war; outlook has grown more daunting

")

Asia-Pacific economies have entered 2026 on a fragile footing, and the US-Israel-Iran war has exacerbated the risks to GDP growth for economies like China, India, and other major countries in the region, says Moody’s Analytics in its latest report.The global economy has been undergoing a period of turmoil since the start of this decade – first it was the Covid pandemic, then the Russia-Ukraine war, then the Donald Trump administration’s tariff policies, and finally 2026 has added the Middle East conflict to the growing list.What does this latest disruption mean for the growth prospects of Asian economies that are in large part dependent on oil and energy imports. Since the start of the Middle East conflict, passage of ships through the Strait of Hormuz has been curtailed, major energy infrastructure across the Gulf has been hit, and oil prices have risen past $100 per barrel, stoking inflation fears.

Fragile Economic Scenario

According to Moody’s Analytics, 2026 was always going to be a tough year for Asia-Pacific countries. Now the uncertainty of the Middle East conflict has added another spanner in the growth wheel of major economies like China, India, Japan, and South Korea.

Growth Across Asia-Pacific Will Slow in 2026

As Moody’s says: Asia-Pacific economies entered 2026 on a fragile footing. Domestic demand was weak, and export growth looked set to slow.“Growth was set to slow after export front-loading ahead of US tariff hikes flattered the numbers last year. And the artificial intelligence boom looked ripe for a pause. Still, cooling inflation allowed some central banks to ease policy, providing reason for cautious optimism. Added to that, the US Supreme Court’s decision in February to strike down country-specific tariffs brought some relief to some of the region’s exporters,” Moody’s Analytics says in its latest report titled ‘Asia-Pacific Outlook: Buckling Up’. But now, recent events have complicated the growth outlook considerably.The report notes the following for major Asian economies:

- External and domestic shocks have scrambled economic fortunes across the region over the past 18 months. Looking at exports, economies seem surprisingly strong, it says, adding that US tariff related uncertainties led to front loading of shipments last year.

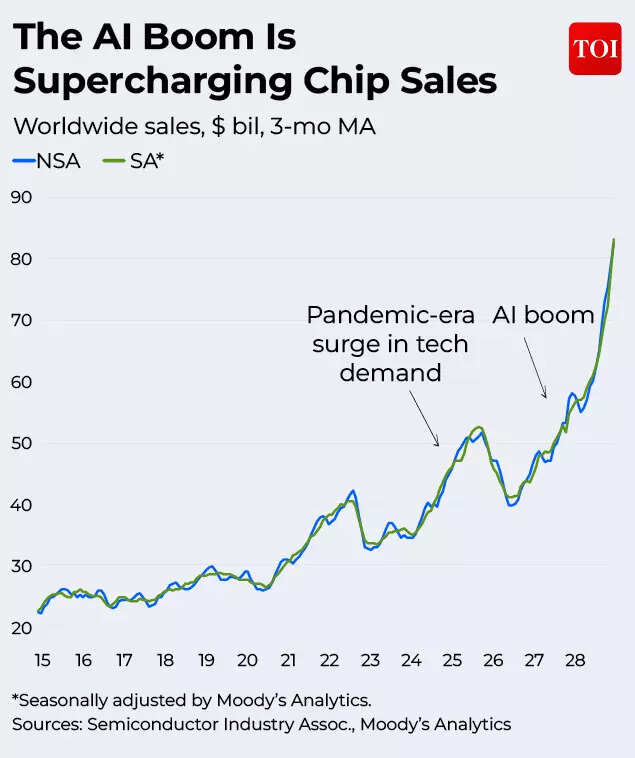

- Shipments of semiconductors, storage and memory related products have grown massively due to the artificial intelligence (AI) -led boom globally. The biggest beneficiary from this has been Taiwan, which has seen a big GDP growth jump of 8.7% in 2025.

- However, according to Moody’s domestic demand has been weak in key economies. “While exports have done well, domestic demand has not. Across much of the region, homegrown demand sits below pre-pandemic trends and global averages, dragging on prices,” it says.

- Consumer price inflation is also averaging below central banks’ target levels. China is actually working to fight off deflation. In India too the CPI is averaging around 3%, below RBI’s 4% target level.

- However, risks to inflation are growing with commodity prices rapidly climbing after the Middle East conflict broke out. “The Middle East conflict is pushing commodity prices higher, raising the possibility that inflation will reaccelerate. It’s also causing shortages of chemicals and fertilisers,” says Moody’s.

“All of this creates an uncomfortable echo of the inflation and supply shocks that followed the COVID-19 pandemic and Russia’s invasion of Ukraine,” it warns.

Three Risks For Asia-Pacific Economies – Where Does India Fit In?

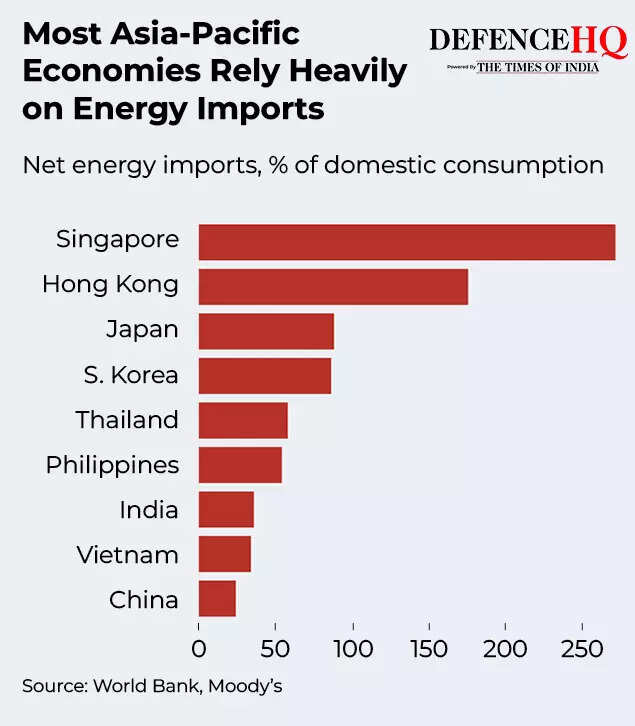

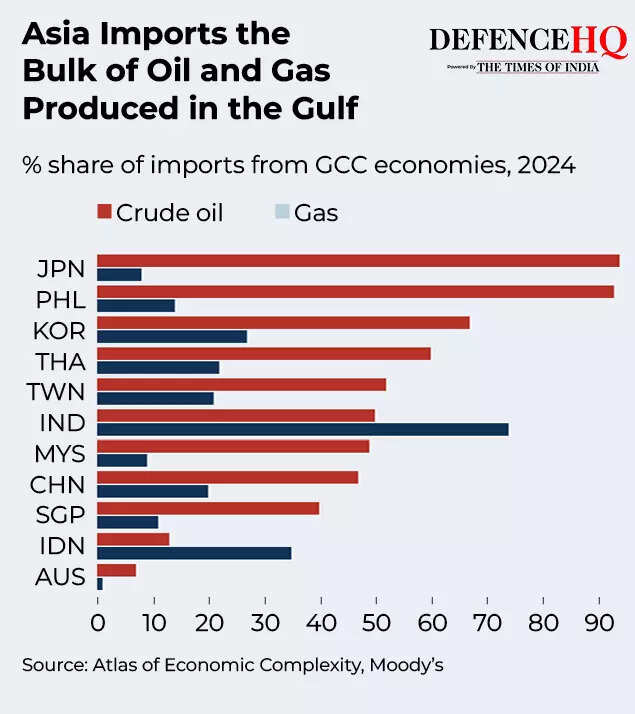

Moody’s has a big warning for Asia-Pacific economies: They are faced with a ‘troublesome mix of external threats’!Threat 1: Middle East ConflictThe report says that the Middle East conflict sits at the top of the list. This is because of the region’s heavy dependence on imported commodities. This is especially true since the source of energy needs is the very set of countries that are currently involved in the conflict.

While India imports a big percentage of its crude oil requirements, Moody’s Analytics is of the view that compared to other countries in the region its dependency is somewhat less.Northeast Asia’s high-income economies such as Japan, South Korea and Taiwan are particularly dependent on imported fossil fuels. However it notes that these countries maintain sizeable strategic oil reserves. The typically limited pass-through from short-lived price spikes to domestic consumer prices provides a meaningful buffer, it says. China, which is one of the largest buyers of Iranian discounted crude, similarly maintains huge reserves.

“India and Southeast Asian economies are somewhat less import-dependent but hold far smaller reserves; their governments instead lean on direct or indirect price caps and fuel subsidy schemes to shield consumers from volatility,” Moody’s Analytics says its report.In a scenario where the US-Iran war does not persist for a longer duration, the inflation shock to South Asian economies would be contained, but a longer breakout of conflict has meaningful implications that cannot be ignored.“A prolonged conflict or a further sustained rise in energy prices would materially alter the assessment of limited impact. In addition to energy prices, food inflation is another concern given its large weight in regional consumption baskets,” the report says.

Threat 2: Trump Tariff RisksMiddle East conflict is not the only risk that threatens the growth story of Asian economies this year. Uncertainty related to tariffs is a big concern.“The Asia-Pacific region has always grown through exports, and that dependence has only deepened since the pandemic. With access to the US market becoming more difficult, the imbalance leaves the region exposed,” says the Moody’s report.The report acknowledges that the US Supreme Court has struck down the Donald Trump administration’s reciprocal tariffs, but quickly points to the 10% global tariff that was announced, with the prospect of it being raised to 15%.

“Trump’s subsequent announcement of a flat global 15% tariff rate means the average effective US import tariff would be broadly unchanged – and considerably higher than this time last year,” it says.The Moody’s report also cautions that the new investigations under Section 301 of the Trade Act signal that the Trump administration is looking to rebuild the tariff regime that existed before the apex court’s decision. Moody’s baseline assumption is that US import tariffs will stay at current levels through 2028.Threat 2: End of the AI Boom?AI has been driving the news for months now – disruptive models are taking the world by a storm, but is the rally set for a pause According to the Moody’s report, a key source of uncertainty around its forecast is the AI boom.“Asia produces most of the world’s electronics, so the surge in AI-related demand has been a powerful tailwind – first in Taiwan, which produces most of the world’s bleeding-edge semiconductors, and since late 2025, in memory chips, storage and related products,” the report notes.

What this has meant is a rise in electronics exports across the region, and an increase in prices and some isolated shortages as well. “Data centre investment has been an added benefit, complementing the export-led growth boost. But this also means the region is heavily exposed should AI momentum falter,” Moody’s says. Exports and investments are at the risk of being hit in case the AI-led boom were to either end or worst still see a big downturn.“Financial markets would react sharply. Nowhere is this dynamic more visible than in South Korea, whose equity market nearly tripled over 18 months before selling off sharply when the Middle East conflict exposed macro vulnerabilities that worsened the risk-off move,” Moody’s explains.

China’s New Economic Normal

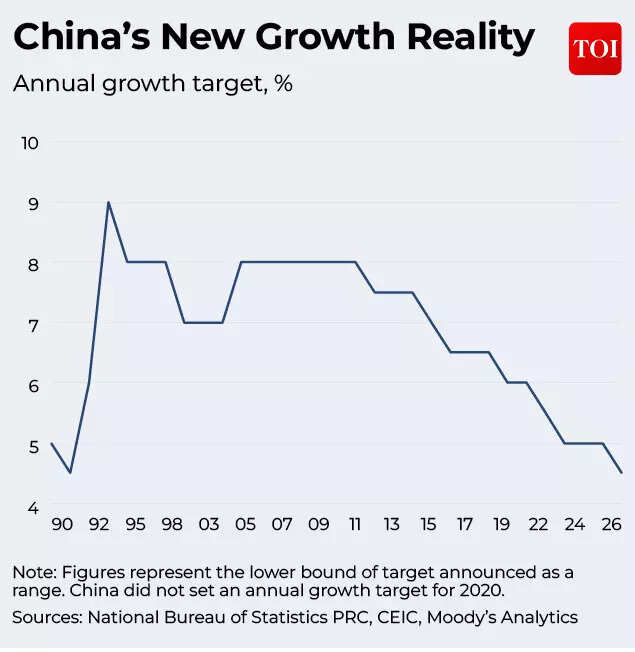

China has been flooding markets with exports, a policy which is driven by its own weak domestic demand. Earlier this month, China projected a GDP growth rate of 4.5% to 5% for 2026 – which is the first time in over three decades that officials in Beijing have projected a sub 5% growth number.Domestic weakness and industrial overcapacity received rhetorical acknowledgement, but the policy focus remains firmly on industrial upgrading and technological self-sufficiency, says Moody’s.

At home, policy efforts to address involution, the excess competition that compresses returns and drives prices ever lower, may be bearing some fruit. But we wouldn’t be surprised if fresh investment into strategic sectors will see involution and deflation return before long, the report says.

South Asia Growth Projections For 2026

With this situation in mind, Moody’s Analytics projects that the growth across the Asia-Pacific region will slow down from 4.3% in 2025 to just 4$ in 2026. The number will come down further to 3.6% in 2027, it estimates.Individual economy wise projections are:

- India: 7.8% in 2025, 7.5% in 2026, 6.2% in 2027, and 6% in 2028

- China: 5% in 2025, 4.4% in 2026, 4.3% in 2027, and 4% in 2028

- Japan: 1.1% in 2025, 0.5% in 2026, 0.7% in 2027, and 0.9% in 2028

- Singapore: 5% in 2025, 3.8% in 2026

- South Korea: 0.9% in 2025, 1.9% in 2026

- Taiwan: 8.7% in 2025, 6.6% in 2026

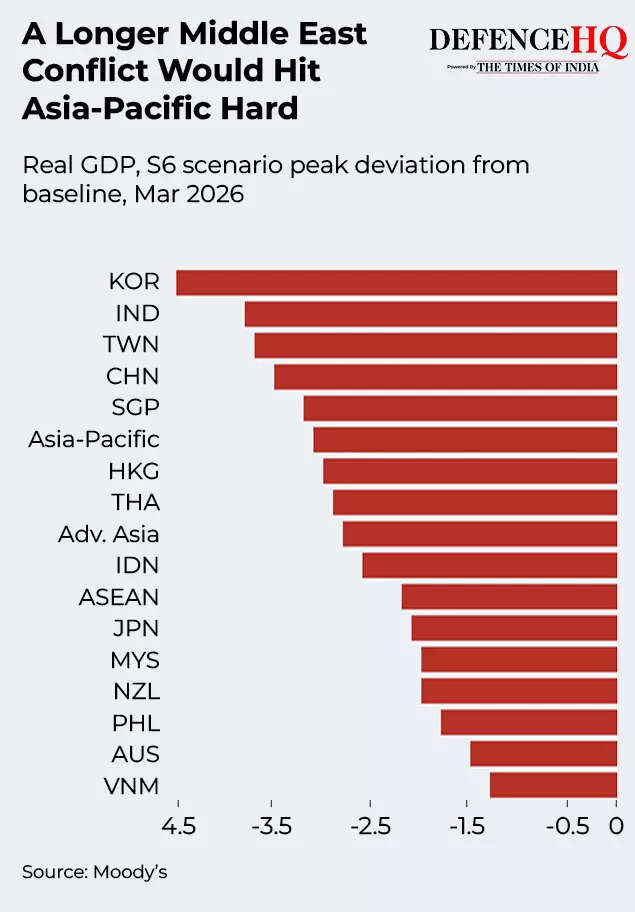

In its report Moody’s Analytics simulates a more ‘severe and protracted’ conflict which sees Brent crude rising substantially.“Results show GDP losses across the APAC region peaking at 3%, a larger hit than either Europe or the US would absorb, reflecting the region’s heavy dependence on Middle Eastern commodities,” it says.

“Developed Asia sustains a particularly large blow; its pronounced exposure to commodity price spikes weakens trade balances and currencies, pushing up inflation. India and China face sizeable damage given their dependence on oil and gas imports from Gulf economies caught up in the conflict,” it adds.As Moody’s Analytics concludes: This year is shaping up to be an even more difficult year for the Asia Pacific region than originally envisaged.“A more severe and prolonged conflict in the Middle East would compound existing tariff pain. And while the AI boom is powering ahead, stretched equity valuations, alongside price spikes and isolated hardware shortages, suggest it is increasingly ripe for a pause. With limited support from fiscal and monetary policymakers, growth will slow,” it says.